Introduction: Your Refund Is Gone Before You Know It

Tax season ends, the refund hits your bank account, and somehow — within a few weeks — it is gone. Sound familiar? You are not alone. Research shows that most Americans spend their entire federal tax refund within 30 days of receiving it, often without any clear memory of where it went.

Here is the thing: your refund is not a windfall. It is your own money — money you overpaid throughout the year — finally returning to you. It deserves a plan.

That is exactly where IRS Form 8888 comes in. This often-overlooked IRS document — officially titled Form 8888, Allocation of Refund — gives you the power to split your refund across multiple accounts automatically, the moment the IRS processes your return. No willpower required. No transfers to remember.

In this article you will learn what Form 8888 is, who it is for, how to use it to cover your tax preparer fees, whether it is actually worth using, and how to fill it out correctly. Let’s make your refund work harder than you ever have.

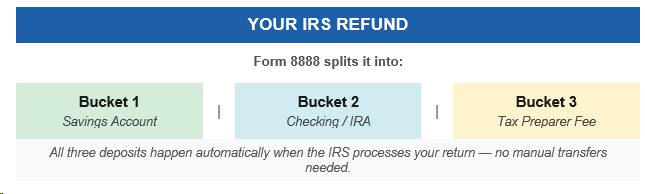

What Is IRS Form 8888? The Tool Most Taxpayers Have Never Heard Of

At its core, IRS Form 8888 is a one-page IRS document that tells the government: “Don’t put my entire refund in just one place.” Instead of a single direct deposit, you direct your refund — or portions of it — to up to three separate bank accounts.

Think of it like setting up automatic bill payments, except the IRS is doing the routing for you. Once you submit your tax return with Form 8888 attached, the split happens automatically with no follow-up needed.

You can use the form to:

- Divide your refund between a checking account and a high-yield savings account

- Send a portion directly to a Roth IRA or traditional IRA

- Pay your tax preparer fees directly from your refund — no separate payment needed

- Route money to a dedicated account for a specific savings goal

IRS Form 8888 attaches to your regular Form 1040 and is processed automatically. It does not slow down your refund and costs nothing to use — it is simply a smarter way to receive money you were already owed.

How Your Refund Travels With IRS Form 8888

Can I Pay My Tax Preparer From My Refund? Yes — Here Is Exactly How

One of the most common questions people ask is: “Can I pay my tax preparer from my refund?” The answer is yes, and it is one of the most practical uses of this form.

The Direct Form 8888 Method

Some tax preparers — especially independent professionals and smaller firms — accept fee payment directly through IRS Form 8888. You list their bank routing and account number in the form, specify the fee amount, and that portion of your refund goes straight to them. The rest lands in your account as usual. Clean, free, and seamless.

The Refund Transfer Method (And Why It Costs More)

Large national chains often use a product called a Refund Transfer (RT). A partner bank temporarily receives your full refund, deducts preparer fees, and sends you the remainder. It looks similar to Form 8888, but there is a key difference: Refund Transfers typically add $30 to $50 in bank processing fees.

Over five years of tax filing, that is $150 to $250 in fees you never had to pay. If your preparer accepts IRS Form 8888 directly, that is almost always the better option. Always ask upfront which method they use.

Is Form 8888 Good or Bad? A Balanced, Honest Take

Searching “form 8888 good or bad” brings up a range of opinions. Here is an objective breakdown so you can make the right call for your situation.

The Case For IRS Form 8888

It builds savings on autopilot. The biggest enemy of saving is friction. Form 8888 removes that friction entirely — money that never passes through your spending account cannot be accidentally spent.

It is completely free. The IRS charges nothing to process a split refund. You get the full benefit of automatic allocation at zero cost.

It supports retirement goals. You can direct part of your refund to an IRA as a prior-year contribution before the tax deadline — one of the simplest ways to boost retirement savings without adjusting your monthly budget.

It reduces the temptation to splurge. Pre-allocating your refund turns a reactive financial habit into a proactive one.

The Case Against — When to Be Careful

Errors delay your refund. A wrong routing or account number can trigger a paper check instead of direct deposit, adding two to three weeks to your wait.

Not all preparers support it. Smaller or newer tax professionals may not be set up to receive fees via Form 8888. Always confirm before counting on it.

Refund Transfer fees catch people off guard. If your preparer uses an RT product and the fees are not made clear upfront, you may receive less than expected. Always read the paperwork.

Verdict: For anyone who wants to be more intentional with their money, IRS Form 8888 is an easy win. The risks are manageable with a bit of care. The upside — automatic savings and zero-cost refund splitting — is real and lasting.

IRS Form 8888 Instructions: How to Fill It Out Correctly

Filling out IRS Form 8888 takes about five minutes once you have your bank account details ready. Here is a plain-English walkthrough of each section.

Part I: Splitting Your Refund Among Up to Three Accounts

For each account you want to receive funds, you will enter:

The bank’s 9-digit routing number (found on the bottom-left corner of a check)

Your account number

Account type: checking or savings

The specific dollar amount going to that account

All amounts must add up to your total refund exactly. If the total is off, the IRS will deposit the difference as a paper check to your mailing address.

⚠ Pro Tip — Double-Check Every Number: A single transposed digit in a routing or account number can send your refund to the wrong account — or trigger a paper check that takes 2–3 extra weeks to arrive. Before filing, verify every number directly with your bank and, if applicable, your tax preparer. The IRS cannot quickly retrieve a misdirected deposit.

Part II: Savings Bonds — Section Removed in 2025

2025 Form Update: As of January 1, 2025, the U.S. Treasury discontinued the option to purchase Series I Savings Bonds through a tax refund. The IRS has removed Part II from the current revision of Form 8888. If you are looking at an older version of the form, this section no longer exists on the current year’s form. To purchase I Bonds, visit TreasuryDirect.gov directly.

Part III: Paying Your Tax Preparer Fees

This section is specifically for directing tax preparer fees from your refund. Enter your preparer’s bank routing number, account number, and the fee amount. Your preparer should supply these details. Once completed, the IRS sends their payment directly — no checks, no transfers, no hassle.

Allocation Refund Strategies: Turn Your Tax Refund Into a Financial Reset

The concept of allocation refund is straightforward: instead of one lump sum disappearing into daily expenses, you pre-decide exactly what each dollar does. It is the financial equivalent of paying yourself first — before spending enters the picture.

The average federal tax refund in the U.S. runs around $3,000. Without a plan, that money tends to vanish. With an allocation strategy and IRS Form 8888, you can turn it into something that lasts all year.

Strategy 1: The Emergency-First Split

Direct 60% of your refund to an emergency savings account and 40% to checking. This one move can fully fund a starter emergency fund — one of the most impactful financial cushions you can build.

Strategy 2: The Debt Destroyer

Route 80% of your refund toward your highest-interest credit card and 20% to savings. You will likely save more in avoided interest charges than any investment return could match.

Strategy 3: The Retirement Accelerator

If you have a Roth IRA and room to contribute, direct a portion of your refund there before the tax filing deadline. This counts as a prior-year contribution — an effortless way to grow retirement savings without touching your monthly paycheck.

Strategy 4: The Goal Fund Builder

Have a specific target — a home down payment, car repair fund, or annual vacation? Open a dedicated savings account and send a fixed percentage there via Form 8888 every year. By the time you need the money, it is already waiting.

IRS Form 8888 is not just a form — it is a system. And systems beat willpower every single time.

Who Should Use IRS Form 8888 This Tax Season?

Form 8888 is not for everyone, but it is right for more people than typically use it. Consider filing it this year if:

- You have trouble saving. If money in checking always finds a way to get spent, automatic allocation changes the game.

- You want to grow your retirement account. A prior-year IRA contribution made from your refund can meaningfully boost your long-term wealth.

- Your tax preparer accepts it. Paying fees from your refund keeps your cash flow intact — especially helpful early in the year when budgets feel tight.

- You have multiple financial goals. Splitting across accounts eliminates the “I’ll transfer it later” trap that derails most financial intentions.

You probably do not need Form 8888 if your refund is going entirely to one account and you are disciplined about transferring savings manually. But if any of the above sounds familiar, it is worth the five minutes it takes to complete.

Conclusion: Stop Letting Your Refund Disappear — Use IRS Form 8888

Most people put more thought into picking a streaming service than planning what to do with thousands of dollars returning to their account each year. That gap between intention and action is exactly what IRS Form 8888 is designed to close.

Whether you want to build an emergency fund, grow your retirement account, cover your tax preparer fees from your refund, or just make sure your savings actually get saved — Form 8888 automates the decision so you do not have to rely on follow-through alone.

It is free, it does not slow your refund, it takes about five minutes to add to your return, and the 2025 form has been streamlined now that the savings bond section has been removed. For the financial peace of mind it delivers, that is one of the best returns on time you will find this tax season.

Ready to put your refund to work? Ask your tax preparer about including Form 8888 this year, or download the latest version directly from IRS.gov/Form8888. A few extra minutes of planning today could mean thousands of dollars in savings, debt reduction, or retirement contributions — starting the moment your refund lands.

This article is for general informational purposes only and does not constitute tax or financial advice. Tax rules change annually — always consult a licensed tax professional for guidance specific to your situation.

Does using Form 8888 delay my refund?

No. The IRS processes Form 8888 as part of your regular return. Adding the form does not extend your wait time. Your refund timeline is the same whether you split across one account or three.

Is Form 8888 required, or is it optional?

It is entirely optional. You only need Form 8888 if you want to split your refund across multiple accounts or direct fees to your tax preparer. For a single-account direct deposit, your Form 1040 handles it without needing Form 8888 at all.

Does Part II of Form 8888 still exist for savings bonds?

No. As of January 1, 2025, the IRS removed the savings bond purchase section from Form 8888. The current revision of the form no longer includes Part II. If you want to invest in Series I Bonds, visit TreasuryDirect.gov to purchase them directly outside of your tax return.