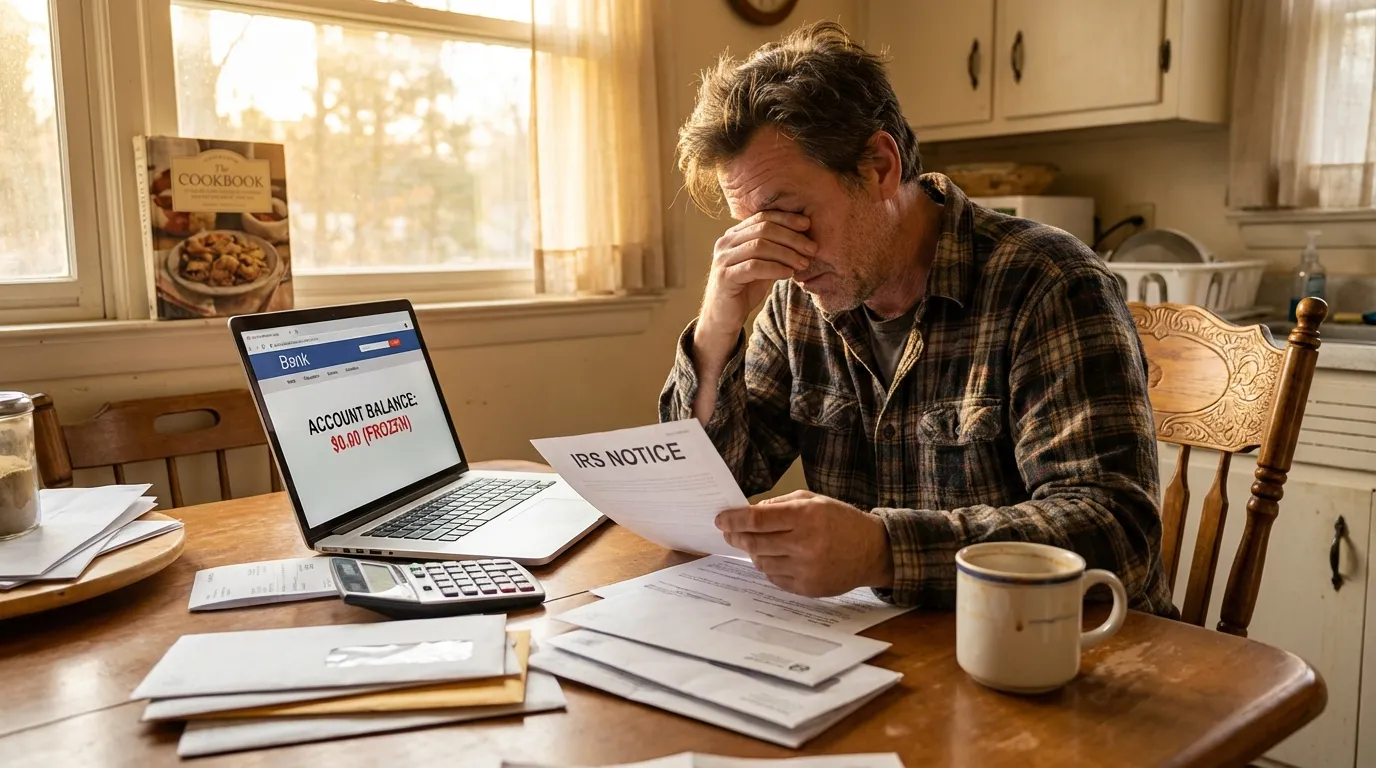

You check your bank account one morning and the balance reads zero. No warning email, no heads-up from your bank. The IRS has placed a levy on your account, and every dollar you had is now frozen. It is one of the most stressful financial situations an American taxpayer can face, and it happens far more often than most people realize.

If you are wondering how to stop an IRS levy, you are not alone. Millions of taxpayers deal with levies, wage garnishments, and asset seizures every year. The good news is that the IRS does not have the final word. There are legitimate, proven ways to get a levy released, prevent future ones, and take back control of your finances.

In this guide, you will learn exactly what an IRS levy is, how it differs from a lien, and the step-by-step strategies that actually work to stop one. Whether the IRS is targeting your bank account, your paycheck, or other assets, this article walks you through every option available to you in 2026.

What Is an IRS Levy and How Does It Work?

Before diving into solutions, it helps to understand what you are actually dealing with. The levies meaning in a tax context is straightforward: a levy is the legal seizure of your property or assets to satisfy a tax debt. It is one of the most aggressive collection tools the IRS has, and it goes well beyond sending you letters.

A levy tax action allows the IRS to take funds directly from your bank accounts, garnish your wages, seize your vehicles, and even claim rental income or accounts receivable if you own a business. The IRS does not need a court order to do this. Once they have followed their internal notification process, they have the legal authority to act.

IRS Levy vs. IRS Lien: Know the Difference

People often confuse levies and liens, but they work very differently. A lien is a legal claim against your property. It tells the world that the IRS has a right to your assets, but it does not actually take them. Think of it as a flag on your financial record. A levy, on the other hand, is the IRS physically taking your money or property. A lien says you owe. A levy takes what you owe.

Understanding this distinction matters because the strategies for dealing with each are different. If you have a lien, you still have your assets. If you have a levy, the clock is already ticking.

Can the IRS Take Money Out of Your Bank Account?

Yes, the IRS absolutely can take money out of your bank account, and it is one of their most commonly used collection methods. When the IRS issues a bank levy, your financial institution is legally required to freeze the funds in your account. After a 21-day holding period, the bank sends those frozen funds directly to the IRS.

During that 21-day window, you cannot access the frozen money. You cannot write checks, use your debit card, or transfer funds. Bills bounce. Rent goes unpaid. It creates an immediate financial emergency for most people.

The bank levy applies to the balance in your account on the day the levy is received. Any deposits made after that date are not included in that particular levy, though the IRS can issue additional levies at any time. This is why speed matters. The moment you learn about a bank levy, you need to act.

How Much of Your Wages Can the IRS Garnish?

Wage garnishment is another common IRS collection tactic, and it works differently than a bank levy. Instead of a one-time freeze, a wage levy is continuous. It stays in effect until the tax debt is fully paid, you reach an agreement with the IRS, or the collection statute expires.

So how much of your wages can the IRS garnish? The answer depends on your filing status and number of dependents. The IRS uses Publication 1494 to determine the exempt amount, which is the portion of your paycheck they cannot touch. Everything above that amount goes straight to the IRS.

For a single taxpayer with no dependents in 2026, the exempt amount is roughly $1,100 to $1,200 per month. That means if you earn $4,000 per month, the IRS could garnish approximately $2,800 of it. For a married taxpayer filing jointly with two children, the exempt amount is higher, but the IRS can still take a significant chunk of your income.

Unlike private creditors, who are typically limited to garnishing 25 percent of disposable income, the IRS has no such cap. They can take far more, which is why an IRS wage garnishment is considered one of the most financially damaging collection actions you can face.

Proven Strategies to Stop an IRS Levy

Now for the part you came here for. If the IRS has issued a levy against your bank account, wages, or other assets, here are the strategies that work in 2026.

1. Pay the Tax Debt in Full

The fastest way to stop an IRS levy is to pay the outstanding balance. Once the debt is satisfied, the IRS is required to release the levy. This is rarely realistic for most taxpayers, but if you can borrow from family, take a personal loan, or liquidate non-essential assets, full payment ends the problem immediately.

2. Set Up an Installment Agreement

If you cannot pay everything at once, an installment agreement lets you pay over time. When the IRS approves a monthly payment plan, they will generally release existing levies. You can apply online through the IRS website for debts under $50,000, or work with a tax professional for larger amounts. The key is demonstrating a willingness to pay and following through on the agreed schedule.

3. Submit an Offer in Compromise

An Offer in Compromise allows you to settle your tax debt for less than what you owe. The IRS accepts these when they determine you genuinely cannot pay the full amount based on your income, expenses, asset equity, and future earning potential. While the IRS reviews your offer, collection activity, including levies, is typically suspended. Approval rates have improved in recent years, but the application process is detailed and having professional help makes a real difference.

4. Request Currently Not Collectible Status

If paying anything right now would create serious financial hardship, you can ask the IRS to classify your account as Currently Not Collectible. This status pauses all collection activity, including levies and wage garnishments. The IRS will review your financial situation and, if they agree you truly cannot pay, they will back off. Your debt does not disappear, and interest continues to accrue, but you get breathing room. The IRS reviews these cases periodically, so your situation will be reassessed down the road.

5. File an Appeal with the IRS

You have the right to appeal a levy through the IRS Collection Due Process hearing. When the IRS sends you a Final Notice of Intent to Levy (typically Letter 1058 or LT11), you have 30 days to request a hearing. During the hearing, you can present alternatives like installment agreements or offers in compromise. While the appeal is pending, the IRS cannot proceed with the levy. This is a powerful tool, but the 30-day window is strict. Miss it, and you lose significant leverage.

6. Prove the Levy Creates Economic Hardship

If the levy prevents you from meeting basic living expenses, such as housing, food, transportation, and medical care, you can request a levy release based on economic hardship. The IRS is required to release a levy if it creates an immediate economic hardship, as defined under Internal Revenue Code Section 6343. You will need to provide detailed financial documentation, but this is one of the most effective approaches for people who are genuinely struggling.

7. Show That the Statute of Limitations Has Expired

The IRS generally has 10 years from the date of assessment to collect a tax debt. This is called the Collection Statute Expiration Date. If the statute has expired, the IRS can no longer legally collect the debt or enforce a levy. Calculating this date can be tricky because certain actions, like filing an Offer in Compromise or filing for bankruptcy, can pause the clock. A tax professional can help you determine if this applies to your case.

How to Protect Yourself From Future IRS Levies

Stopping a current levy is urgent, but preventing the next one is equally important. The IRS rarely jumps straight to a levy. There is usually a series of notices that escalates over weeks or months before they take action. Responding early is the single best way to avoid a levy altogether.

Always open IRS mail. It sounds obvious, but many taxpayers ignore letters from the IRS out of fear or anxiety. Every piece of IRS correspondence is a chance to resolve the issue before it escalates. If you receive a CP504 notice, which is the final notice before levy action, treat it as an emergency.

File your tax returns on time, even if you cannot pay. The IRS treats non-filers much more aggressively than taxpayers who file but owe a balance. Filing shows good faith, and it opens the door to payment plans and other resolution options.

Keep your address updated with the IRS. If they send notices to an old address and you never receive them, the IRS can still proceed with collection. The law only requires them to send the notice, not to confirm you received it.

When to Hire a Tax Professional

You can handle some levy situations on your own, particularly if the amount is small or if you are eligible for a straightforward installment agreement. But if your tax debt is large, involves multiple years, or the IRS has already begun seizing assets, working with a qualified tax professional is strongly recommended.

Enrolled agents, CPAs, and tax attorneys all have the authority to represent you before the IRS. They can negotiate directly with revenue officers, file appeals on your behalf, and identify resolution strategies you might not know about. Many offer free consultations, so there is no risk in exploring your options.

Be cautious of companies that make unrealistic promises, like guaranteeing they can settle your debt for pennies on the dollar. Legitimate tax professionals will give you an honest assessment of your situation and outline realistic outcomes.

Take Action Now to Stop an IRS Levy

Dealing with an IRS levy is stressful, but it is not a dead end. Whether the IRS has placed a bank levy on your account, started garnishing your wages, or sent you a final notice, you have options. From installment agreements and offers in compromise to hardship claims and appeals, the strategies outlined in this guide give you a clear path forward.

The most important thing you can do right now is act. The longer you wait, the fewer options you have. If you are unsure where to start, contact a qualified tax professional for a free consultation. They can review your specific situation, explain your rights, and help you choose the best strategy to stop the levy and get your financial life back on track.

Do not let the IRS dictate your financial future. Take the first step today.

FAQ

How long does it take to get an IRS levy released?

It depends on the method. Paying in full can result in a release within days. An installment agreement typically takes two to four weeks once approved. Offers in Compromise can take several months to process, but collection is usually paused while the IRS reviews your case. If you prove economic hardship, the IRS can release a levy relatively quickly, sometimes within a few business days.

Can the IRS levy my joint bank account?

Yes. If you have a joint bank account and the IRS issues a levy against you, the entire account can be frozen. Your co-account holder can file a claim with the IRS to recover their portion of the funds, but this process takes time and requires documentation proving which funds belong to them.

Does an IRS levy affect my credit score?

A levy itself does not appear on your credit report. However, a federal tax lien, which often accompanies a levy, can significantly damage your credit. Additionally, the financial fallout from a levy, such as bounced checks, missed payments, and overdraft fees, can indirectly harm your credit standing.